What is $200 to you?

To a wealthy person, it is probably loose change. On the other end of the spectrum, the same amount could very likely feed an entire family for a month.

Money has always been a concern in our lives. After all, it is the only tangible currency that dictates our lifestyle. That is, unless you lead an ascetic life.

For average citizens like you and me, the ever increasing costs of living in Singapore continues to be a worry and that little voice nagging at the back of our minds every time we spend.

A lot of us also grapple with the fear of not being able to ‘afford our life' when we grow old, frail, and sickly. But when I look at how our mothers (and fathers) have saved up very decent (five-figure) sums of money not just for themselves but also for us, their children, it makes me wonder: How the heck did they do it?

Considering the circumstances in which our parents grew up made me genuinely wonder why we struggle with finances now. With the generally lower income they would have drawn compared to our salaries today, it should not be too difficult for us to achieve the same kind of financial stability and still lead a fairly comfortable lifestyle, right?

Maybe not.

Awhile back, I penned my thoughts on my future in Singapore, where I shared the fears I have and the uncertainty of whether I’d be able to afford (a graceful) retirement in Singapore. To which I believe is the same concern felt by many Singaporeans.

Over the last couple of months however, life milestones like marriage and home ownership has made me realise how clueless I had been with money.

Yes, of course. There are many factors to consider. Our policies, the ten-fold increase in housing prices, and inflation are all changes that has made it more challenging for us. But these are all areas that we have no control over, and are complex topics to debate over as itself.

On a more personal level, I have come to realise how little we know about money and affordability in our day-to-day lives.

“What does it mean to live within our means?”

It's a question that is so important, yet so hard to answer.

A lot of us spend based on our whim and fancy, not caring too much about whether we can afford it or not. Or rather, we spend based on a very vague assessment of whether we will be able to afford our meals (and necessities) for the rest of the month without going ‘broke’.

The problem with this is that when you add personal desire into the equation, you can bid logic and pragmatism goodbye.

Take for instance how we will usually avoid spending more than $20 on a meal, but we wouldn’t hesitate to spend $200 on a ticket to watch our favourite artiste live in concert.

It's exactly what 29-year-old Zafirah would do. $200 can be used to finance two to three weeks worth of her expenses, but like many Singaporeans, her spending is also very sporadic. As another millennial I spoke to explained, the amount he spends “is totally proportionate to how much of a life I have that week.”

While Zafirah avoids spending too much on lunches, she is willing to splurge on special occasions like birthdays and anniversaries, as well as concerts of her favourite artistes and on holidays.

“Beyond the price I look more at whether it's value-for-money. Even if I splurge or 'go big', I try to find vouchers and promos to reduce my spending. Like right now, I'm eyeing the Dyson Airwrap but I just can't justify spending $600 on a hairdryer.”

All of us attach a different value to the same amount of money, and even on the same amount of money, we perceive value differently based on context.

Take for instance a literal comparison of apple to apple. $5 apples Vs. $55 premium apples. The $50 difference is a lot for fruits. However, $50 is not that big of a deal if you’re comparing long-haul flight tickets, and nothing when you’re looking at housing prices.

There are also those who end up being in debt for years after spending a bomb on achieving their dreams, like a dream wedding—a once in a lifetime affair. A 2016 TNP article shared the struggles faced by a couple who spent $110K on their big day, which left them with a four-year debt.

Is the $110k considered affordable or not then?

Because the value of money is so intangible, it is very hard not to have a biased perception of value, which makes it very hard to discern whether one can really afford something or not. Personal preference, the context of which we're spending, and our earning power all affects our perception of value.

With plenty of payment options and interest-free instalment plans easily available today, the line between affordable and not over-budget isn't clear anymore. We’d all like to think that we are sensible enough to know what we can and cannot afford. But we probably don’t.

We spend on our whim and fancy because there has never been immediate pressure for us to save. For the majority of us, it is a fact that we have lived a sheltered life and never faced a real fear of not having enough to get through another day.

Financial literacy isn’t natural to us either. The only thing we’ve been taught is to save for a rainy day, period. As we grow older, we just grasp for information in the dark, trying to find out about the best savings account and plans, and financial planning tips through Google, friends, financial advisors, and through trial and error.

In our daily lives, we often blurt out the occasional “I can’t afford this.” But I’d make the bold claim that one will only truly know what one can or cannot afford when faced with either having to pay off student loans independently, or when one is getting married and buying a house.

From young, my mother has always stressed this to me: Every dollar counts. When I started working however, I began to lax on that principle. The liberating freedom of seeing 4-figure amounts deposited into my bank account every month gave me the false impression that I can afford luxuries.

There’s always that tiny voice at the back of my head that continues to make me feel guilty for splurging, but on most occasions, the lure of gratification is way too enticing, especially when it comes to food. Not forgetting the FOMO on trends: the seasonal McDonald's burgers, the carnivals, the countless new bubble tea brands in Singapore, and basically anything that's on everyone's Instagram at any certain period of time.

The scariest part is when everything is digital, because it is way too easy to just swipe the card and worry about the money later.

Honestly, it is only after having to pay for a wedding banquet and a house that made me truly realise how careless I have been with my money. And this is probably the same for many of us and going to be the same for many more of us.

It is when you put things into perspective, like how the bill of a wedding banquet alone can be 20 to 30 months of your take-home pay, when you realise how f**ked you are in terms of your finances.

Until then, enjoy all the little luxuries while it lasts.

This is not a sponsored post.

Also read: Are Young Couples Jumping Onto The BTO Bandwagon Too Soon?.

(Header Image Credit: Fabian Blank on Unsplash)

GIF from GIPHY

The fact that it is such a foreign concept also made me think of the worst that can happen, and I sure as hell didn’t want to end up bankrupt from uninformed investment choices at such a young age.

GIF from GIPHY

The fact that it is such a foreign concept also made me think of the worst that can happen, and I sure as hell didn’t want to end up bankrupt from uninformed investment choices at such a young age.

GIF from GIPHY

However, like what DollarsAndSense.sg wrote in an article about investing with just $100 a month in Singapore, “Setting aside a large sum of money and acquiring extensive knowledge before you actually start investing is not only unnecessary and impractical, it may not even be the ideal situation.”

As for 26-year-old Billy who paid to learn from investment courses, his challenges were figuring out what stocks to buy and which platform to use when he first got started at 22. And it was a nerve-wrecking process of trial and error before he got the hang of things.

Even for Daniel and Billy today, they still find themselves lacking time to monitor their investments.

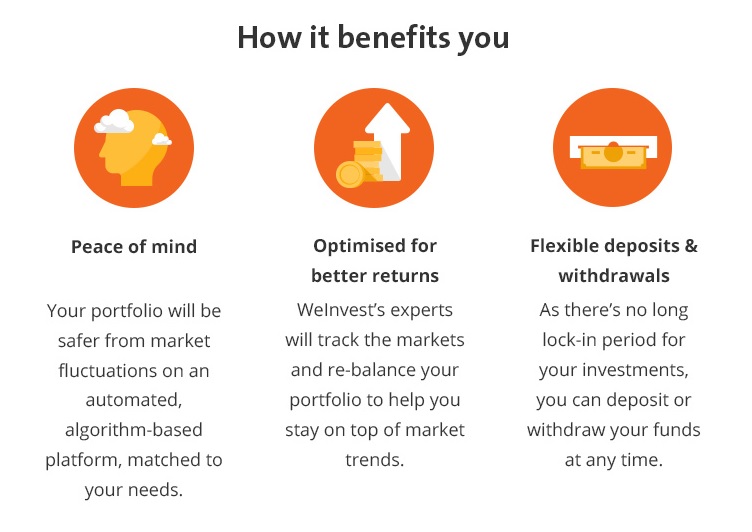

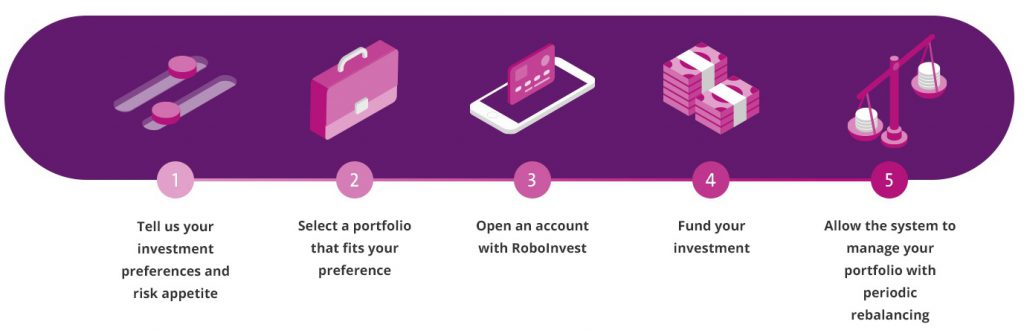

That’s where technology like the new robo-investing service comes in.

GIF from GIPHY

However, like what DollarsAndSense.sg wrote in an article about investing with just $100 a month in Singapore, “Setting aside a large sum of money and acquiring extensive knowledge before you actually start investing is not only unnecessary and impractical, it may not even be the ideal situation.”

As for 26-year-old Billy who paid to learn from investment courses, his challenges were figuring out what stocks to buy and which platform to use when he first got started at 22. And it was a nerve-wrecking process of trial and error before he got the hang of things.

Even for Daniel and Billy today, they still find themselves lacking time to monitor their investments.

That’s where technology like the new robo-investing service comes in.